Advance Tax (1st Installment)

1. All taxpayers (salaried, freelancers, and businesses) whose estimated net tax liability for the Financial Year 2026–27 exceeds Rs. 10,000 after accounting for TDS. Taxpayers must calculate and deposit a minimum of 15% of their total estimated tax liability for the year. This is the first of the four quarterly advance tax installments. Impact of Non-Compliance- Failure to pay or short-payment of this installment attracts a statutory interest penalty of 1% per month under Section 234C for the period of the shortfall.

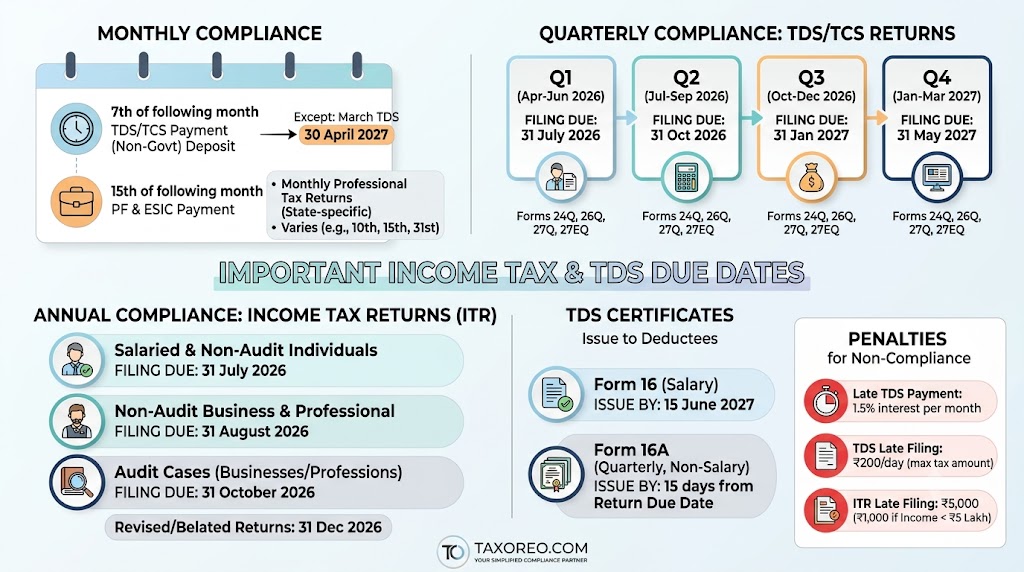

2. Form 16 / 16A Issuance DeadlineDue Date: June 15, 2026: All employers (corporate and non-corporate) and deductors who have deducted Tax Deducted at Source (TDS) during the final quarter of the financial year ending March 31, 2026. Requirement Form 16: Employers must issue this certificate to their employees, reflecting total salary paid and the exact amount of TDS deducted during FY 2025–26. Form 16A: Deductors must issue this quarterly certificate to vendors/contractors for non-salary payments (like professional fees, rent, or interest) where tax was deducted.Impact of Non-Compliance: Delay in issuing these mandatory certificates results in a statutory penalty of Rs. 100 per day for each day the default continues, subject to a maximum cap of the total TDS amount deducted. It also prevents deductees from matching records in their Annual Information Statement (AIS) or Form 26AS to timely file their Income Tax Returns (ITR).