GST & E-Way Bill: New Rules Effective June 15

E-Way Bill Changes Effective 15-June-2026

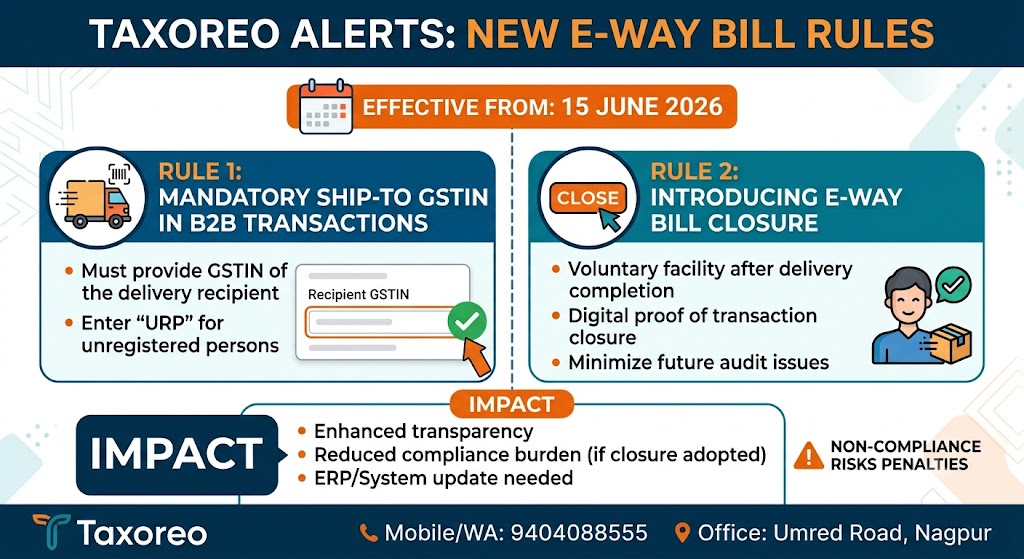

Mandatory Ship-To GSTIN & Closure FacilityPublished on: 09-Jun-2026The Goods and Services Tax Network (GSTN) has announced two significant enhancements to the e-Way Bill (EWB) portal that will come into effect from June 15, 2026. These changes are designed to improve data integrity, boost the traceability of consignments, and stream line the transaction life cycle.Here are the key updates every taxpayer, supplier, and transporter needs to know to avoid transit delays or non-compliance penalties:

1. Mandatory "Ship-To" GSTIN for Bill-To / Ship-To TransactionsIn a Bill-To / Ship-To arrangement (where goods are billed to one entity but physically delivered to a different location or party), leaving the delivery recipient's GSTIN field blank will no longer be permitted.

The Rule: The portal will strictly require the GSTIN of the actual consignee receiving the goods.

For Unregistered Recipients: If the delivery recipient or final destination is an individual or unregistered entity, taxpayers must enter "URP" (Unregistered Person) in the Ship-To GSTIN field.

Impact: Mismatched or blank fields will trigger validation errors, completely halting e-Way Bill generation and potentially delaying dispatches.

2. New Voluntary E-Way Bill Closure FacilityGSTN is rolling out an official transaction closure feature on the production portal. Previously, users could only generate or cancel an e-Way Bill.

The Rule: Suppliers, recipients, transporters, or authorized drivers can now formally mark an e-Way Bill as "Closed" via the common portal or API integration after successful delivery.

Status: This facility is voluntary for now; businesses will face no penalties if they do not use it immediately.

1 However, early adoption is highly recommended as it creates a digital delivery proof that drastically reduces future record-matching and audit disputes.

Quick Comparison: Cancellation vs. Closure

| Particular | Cancellation | Closure |

| Purpose | Used when EWB is faulty or goods are not transported. | Used after successful physical delivery of goods. |

| Stage | Before or during the movement of goods. | Positively after the delivery has been completed. |

| Effect | Renders the e-Way Bill invalid. | Marks the e-Way Bill status as "Completed." |

| Time Limit | Must be done within 24 hours of generation. | To be performed post-delivery within GSTN timelines. |

Compliance Reminder: Non-compliance or transporting taxable goods without a valid, properly filled e-Way Bill attracts a penalty of Rs. 10,000 or the tax sought to be evaded, whichever is higher, under Section 122 of the CGST Act.