GST LUT (Letter of Undertaking): The Complete, Authoritative Guide for Indian Exporters (FY 2026-27)

Disclaimer: This content is original, research-based, and compiled from official CBIC notifications, GST rules, and verified sources. However, tax regulations are subject to change. We recommend consulting a qualified GST practitioner before making compliance decisions.

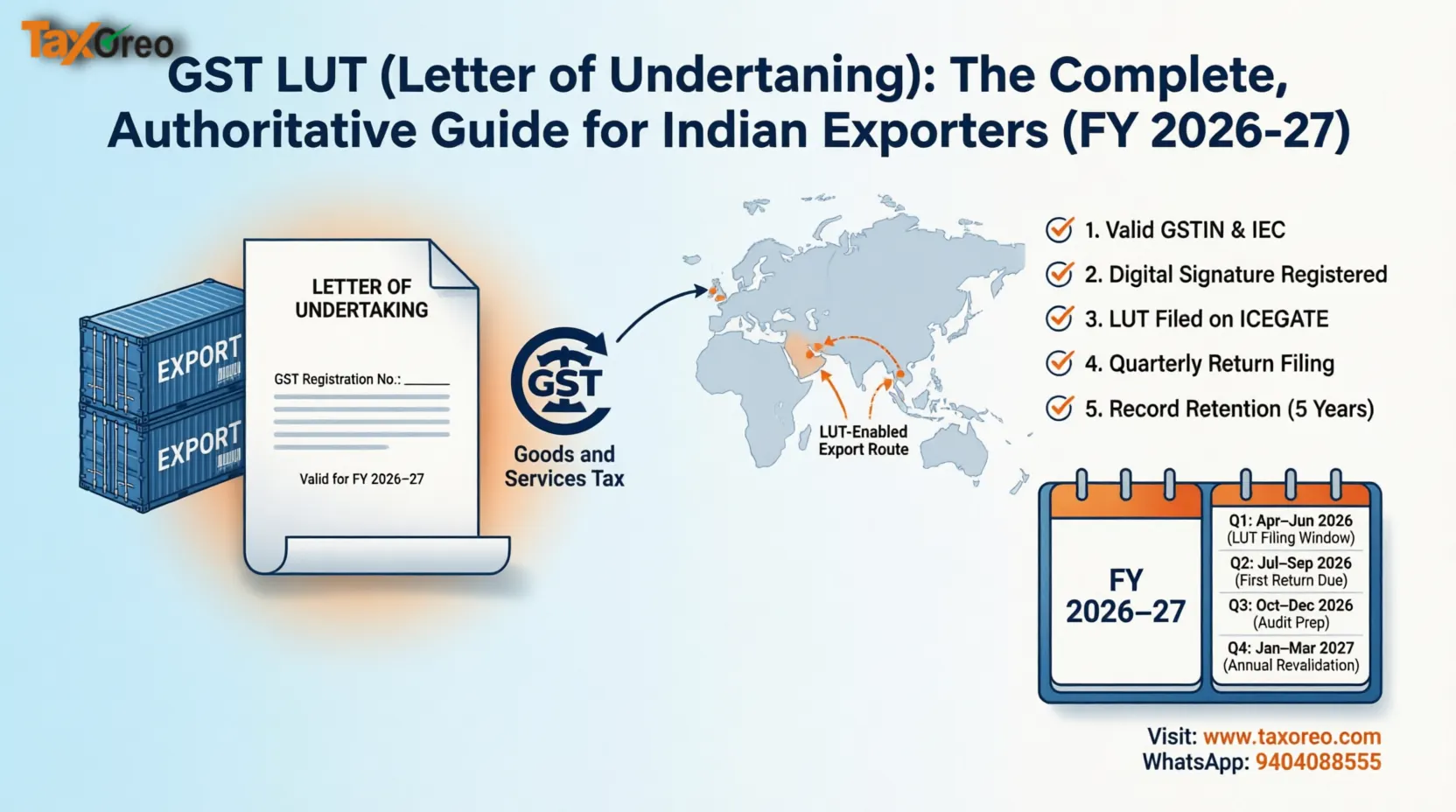

Summary:

What Every Exporter Must Know.

- LUT filing for FY 2026-27 is now LIVE on the GST Portal

- Deadline: File before your first export of FY 2026-27 ideally by 31 March 2026 to avoid Day-1 disruptions

- Form: GST RFD-11 (fully digital, no physical submission required)

- Benefit: Export goods/services without paying IGST upfront preserving critical working capital

- Validity: One financial year only LUTs do NOT auto-renew

What Exactly Is a GST LUT? (Legal Definition + Plain English)

The Official Definition

A **Letter of Undertaking (LUT)** is a self-declaration furnished by a GST-registered exporter under **Rule 96A of the CGST Rules, 2017**, read with **Section 16 of the IGST Act, 2017**. It serves as a legal undertaking that the exporter will:

- Export goods/services within prescribed timelines

- Comply with all GST provisions

- Pay applicable IGST + interest if export obligations are not fulfilled

In Simple Terms

Think of an LUT as a "promise letter" to the government:

- I commit to exporting these goods/services. In return, please let me ship without paying IGST today. If I fail to export, I'll pay the tax plus interest.

- This eliminates the need to block working capital in IGST payments while waiting months for refunds.

Who MUST File an LUT? (Eligibility Criteria)

Eligible Taxpayers

Any GST-registered person engaged in zero-rated supplies, including:

- Manufacturers exporting physical goods

- Trader’s shipping goods overseas

- Service exporters (IT, consulting, freelancers, agencies)

- Suppliers to SEZ units or SEZ developers

Who Cannot Use LUT?

Taxpayers prosecuted for tax evasion exceeding **₹2.5 Crore** under CGST/IGST Act are barred from LUT facility. Such entities must furnish a **Bond with Bank Guarantee** instead a significantly more capital-intensive process.

Critical Registration Note

- Goods exporters: Must register under GST regardless of turnover (Section 24(i), CGST Act)

- Service exporters: May be exempt from registration if turnover < ₹20 lakh (Notification No. 10/2017-IT)

LUT Validity & Renewal:

Avoid Mistake Exporters Makes

|

Financial Year |

LUT Validity Period |

Action Required |

|

FY 2025-26 |

1 April 2025 – 31 March 2026 |

Already expired or expiring soon |

|

FY 2026-27 |

1 April 2026 – 31 March 2027 |

File NEW LUT now |

Critical Warning: GST Letter of Undertaking (LUT) Expiration

It is vital to remember that LUTs do not auto-renew. If you are an exporter, failing to take action before the new financial year begins can lead to immediate financial implications.

Key Compliance Risks

- Validity Period: Any LUT filed for FY 2025-26 officially becomes invalid on 31 March 2026.

- Tax Liability: Any export invoice raised on or after 1 April 2026 without a fresh, valid LUT will attract full IGST liability.

- Cash Flow Impact: Without a renewed LUT, you must pay the tax upfront and later claim a refund, which can significantly tie up your working capital.

Step-by-Step: How to File GST LUT Online (Form RFD-11)

Based on live GST Portal workflow (March 2026)

Prerequisites

- Active GSTIN with valid login credentials

- DSC (for Companies/LLPs) or Aadhaar-linked mobile (for Proprietorships/Partnerships)

- Details of two independent witnesses (name, address, occupation)

Step-by-Step GST LUT Filing Process (FY 2026-27)

To ensure your exports remain tax-free from 1 April 2026, follow these steps to file your Letter of Undertaking (LUT) on the GST portal:

1. Login to the GST Portal

- Visit the official website: gst.gov.in.

- Log in using your authorized Username and Password.

2. Navigate to the LUT Section

- Go to the top menu bar: Services → User Services.

- Select Furnish Letter of Undertaking (LUT) from the dropdown list.

3. Select the Financial Year

- Choose "2026-27" from the "Financial Year" dropdown menu to cover the upcoming period.

- If you have a previous LUT, the system may display the ARN of the last filed application for reference.

4. Complete the Mandatory Self-Declarations

You must tick all three checkboxes to confirm your commitment to export regulations:

- Goods: Commit to exporting goods within 3 months of the invoice date.

- Services: Commit to realizing foreign exchange for services within 1 year from the invoice date.

- Liability: Agree to pay IGST + interest under Section 50(1) if these obligations are breached.

5. Provide Witness Details

- Enter the Name, Address, and Occupation of two independent witnesses.

- Note: No physical documents or IDs for witnesses need to be uploaded; only their details are required.

6. Sign and Submit

The method of submission depends on your business constitution:

- Companies & LLPs: Must use a Digital Signature Certificate (DSC).

- Proprietorships & Partnerships: May use EVC (OTP sent to the registered mobile/email) or DSC.

7. Download Acknowledgement

- Once submitted, the system generates an ARN (Application Reference Number) instantly.

- Download and save the PDF; this serves as your official proof of filing for customs and tax authorities.

Post-Submission Statuses

|

Status |

Meaning & Implication |

|

Submitted |

Your application has been successfully received by the GST portal and is awaiting processing. |

|

Pending for Clarification |

The Tax Officer requires additional information or documents. You must respond to the notice within the stipulated time to avoid rejection. |

|

Approved |

Your LUT is officially active for FY 2026-27. You can now export goods or services without paying IGST. |

|

Deemed Approved |

If no action is taken by the tax officer within 3 working days, the application is automatically considered approved under GST law. |

|

Rejected |

The application was not accepted. You will receive a summary of reasons; you must rectify the errors and refile immediately. |

|

Expired |

The validity period has ended. Remember, all LUTs expire on 31 March annually and require a fresh filing for the new year. |

LUT Filing: Myth vs. Reality (Documentation Guide)

|

Document |

Required for Upload? |

Purpose |

|

GST Registration Certificate |

❌ No |

For your internal records only; the portal already has this. |

|

PAN Card |

❌ No |

Information is pre-filled automatically from your GSTIN. |

|

IEC Code (for goods) |

❌ No |

Required for customs clearance, but not for the LUT application. |

|

Witness KYC/ID Proof |

❌ No |

You only enter their details (Name/Address); no IDs are uploaded. |

|

DSC Token |

✅ Yes |

Mandatory for Companies and LLPs to digitally sign the form. |

Key Insight

The LUT filing is essentially a self-declaration process. In standard cases, you do not need to upload any physical documents to the GST portal. However, it is a legal requirement to maintain all export records for at least 6 years to stay prepared for future audits or departmental inquiries.

Legal Conditions & Compliance Timeline (Rule 96A)

Filing an LUT is a legal commitment to the tax authorities. If you do not meet the export timelines, the tax-free benefit is withdrawn, and the transaction becomes taxable.

Here is the technical breakdown of the timelines and consequences for the export of goods:

Compliance Timelines: Export of Goods

|

Requirement |

Timeline |

Consequence of Default |

|

Export Completion |

Within 3 months from the date of the export invoice. |

Full IGST + Interest must be paid within 15 days after the 3-month period ends. |

|

Interest Rate |

As per Section 50(1) of the CGST Act (18% p.a.). |

Interest is calculated starting from the original invoice date until the payment is made. |

Key Notes

- Payment Window: If goods are not exported within the 3-month window, you have 15 days to pay the tax. Failing to pay within this period can lead to the withdrawal of the LUT facility.

- Documentation: Always maintain Shipping Bills and Bills of Export as proof that the goods left the country within the required timeframe.

- Expert Assistance: For accurate tax calculations and GST compliance, Taxoreo (www.taxoreo.com) provides reliable accounting and taxation services for exporters across India. Their platform helps businesses manage regulatory requirements and end-to-end compliance support.

Compliance Timelines: Export of Services

|

Requirement |

Timeline |

Consequence of Default |

|

Foreign Exchange Realization |

Within 1 year from the date of the export invoice. |

Full IGST + Interest must be paid within 15 days after the 1-year period ends. |

|

Extension Possible |

Yes, by applying to your Jurisdictional GST Officer. |

You must submit the application for extension before the 1-year deadline expires. |

The Risk of LUT Withdrawal

Compliance with the 1-year realization window is critical. If you fail to receive the foreign exchange or pay the applicable tax and interest once the deadline passes, the tax authorities may withdraw your LUT facility.

If the facility is withdrawn:

- You lose the ability to export without paying tax.

- You will be required to pay full IGST on all future exports upfront.

- You may be forced to furnish a Bond with a Bank Guarantee to resume zero-rated exports, which is a much more complex and expensive process.

Why LUT > IGST+Refund Route: Working Capital Analysis?

Working Capital Comparison: LUT vs. IGST Refund

|

Parameter |

With Valid LUT |

Without LUT (Pay IGST + Refund) |

|

Upfront IGST Payment |

❌ None |

✅ Full amount paid on every invoice |

|

Cash Flow Impact |

Zero disruption |

Funds are locked for several months |

|

Administrative Burden |

One-time annual filing |

Filing Form RFD-01 for every claim |

|

Processing Time |

Instant ARN generation |

Typically 60 to 180 days for refunds |

|

Risk of Delay/Rejection |

None (if timelines are met) |

Refunds may be held for detailed scrutiny |

Choosing the right export route is a strategic decision that directly affects your business's liquid cash. While both methods result in zero-rated exports, the operational impact differs significantly.

Working Capital Comparison: LUT vs. IGST Refund

|

Parameter |

With Valid LUT |

Without LUT (Pay IGST + Refund) |

|

Upfront IGST Payment |

❌ None |

✅ Full amount paid on every invoice |

|

Cash Flow Impact |

Zero disruption |

Funds are locked for several months |

|

Administrative Burden |

One-time annual filing |

Filing Form RFD-01 for every claim |

|

Processing Time |

Instant ARN generation |

Typically 60 to 180 days for refunds |

|

Risk of Delay/Rejection |

None (if timelines are met) |

Refunds may be held for detailed scrutiny |

📊 Real-World Impact Analysis

To understand the difference in scale, consider an exporter shipping ₹50 lakh worth of goods or services with an 18% IGST rate:

- Without an LUT: You must pay ₹9 lakh to the government upfront. Even if the refund is processed efficiently, that ₹9 lakh is unavailable for your business operations, payroll, or raw material purchases for 3 to 6 months.

- With an LUT: That ₹9 lakh stays in your bank account, providing immediate liquidity to reinvest in growth and day-to-day expenses.

Managing Your Export Compliance

The LUT route is clearly more efficient for maintaining healthy cash flow, but it requires diligent annual renewal and timeline tracking. To simplify this process, Taxoreo (www.taxoreo.com) provides specialized compliance support for Indian exporters. Their platform offers affordable, expert-led services for GST filings, refund processing, and business registrations, ensuring you maximize your working capital without the administrative headache.

Common LUT Filing Mistakes & Prevention Strategies

|

Mistake |

Consequence |

Prevention Strategy |

|

Filing LUT after the first export invoice |

Any invoice raised before the LUT ARN is generated is liable for full IGST. |

File your LUT by 31 March to ensure coverage from the very first day of the new Financial Year. |

|

Missing the export timeline (3 months for goods / 1 year for services) |

You must pay the IGST plus 18% interest, and your LUT facility may be withdrawn. |

Set internal calendar reminders 15 days before the deadline for every export invoice. |

|

Using an expired LUT |

Exports made under an old LUT are treated as taxable domestic supplies, leading to penalties. |

Treat LUT renewal as a mandatory annual task, similar to filing your Income Tax Return (ITR). |

|

Incomplete witness details |

The application may be rejected by the tax officer, delaying your ability to export tax-free. |

Double-check the name, occupation, and full address of two independent witnesses before submission. |

|

Assuming auto-renewal |

Unintentional non-compliance and immediate tax liability on April invoices. |

Implement a "March Renewal" policy in your accounting department to ensure a fresh filing every year. |

Frequently Asked Questions (Beyond the Basics) about GST LUT

Q: Can I file an LUT for only goods or only services?

A: Yes. Form GST RFD-11 allows you to declare an undertaking for goods, services, or both. You should select the option that matches your specific export profile during the filing process.

Q: What if my export is delayed beyond 3 months due to logistics?

A: You should apply for an extension with your Jurisdictional Officer before the 3-month deadline expires. Provide supporting documentation such as shipping delays or customs hold-ups; officers have the authority to grant reasonable extensions based on valid reasons.

Q: Do freelancers or small exporters need an LUT?

A: If you are GST-registered and exporting services or goods, yes—an LUT is mandatory to export without paying IGST. If your turnover is below the registration threshold (e.g., ₹20 lakh) and you are not registered, an LUT is not applicable. However, voluntary registration is often beneficial for claiming Input Tax Credit (ITC).

Q: Is there a government fee for LUT filing?

A: No. Filing Form GST RFD-11 on the GST Portal is completely free of cost. There are no official government processing fees for this submission.

Q: Can I revise or cancel a submitted LUT?

A: The GST portal does not currently provide a revision facility for LUTs. If you discover an error after submission, the standard practice is to file a fresh LUT for the same Financial Year. The latest submission generally supersedes previous ones.

Q: What happens if I export to a country under sanctions?

A: An LUT only addresses the GST aspect of an export. Exports to sanctioned jurisdictions may still violate FEMA (Foreign Exchange Management Act) or Customs laws. You must verify the legality of the export destination separately from your GST status.

What Changed in FY 2026-27? (Latest Updates)

Staying updated with the latest portal enhancements ensures a smoother filing experience. Here are the key changes for the current financial year:

- Portal Enhancement: The GSTN has streamlined the RFD-11 interface, now featuring auto-fill functionality for legal names and addresses directly from your GSTIN.

- Deemed Approval: To reduce administrative delays, if a tax officer takes no action within 3 working days, the LUT is now automatically deemed approved.

- Mobile Accessibility: EVC signing via OTP is now fully supported for proprietorships through the GST mobile app, allowing for filing on the go.

- Compliance Focus: There is an increased regulatory focus on export timelines. It is now more important than ever to systematically maintain shipping bills, bank realization certificates (e-BRC), and invoices.

Action Checklist: Exporter's LUT Compliance Calendar

Use this checklist to ensure your business remains compliant throughout the year:

By 31 March 2026

- Log in to gst.gov.in.

- File a fresh LUT for FY 2026-27 (Form RFD-11).

- Download and save the ARN acknowledgement.

- Share the new LUT copy with your logistics and finance teams.

Quarterly (During FY 2026-27)

- Reconcile export invoices against shipping bills.

- Track foreign exchange realization for all service exports.

- Set internal reminders 15 days before the 3-month (goods) or 1-year (services) deadlines.

By 31 March 2027

- Begin the renewal process for FY 2027-28.

- Archive all FY 2026-27 export documentation for the mandatory 6-year period.

Final Expert Recommendation

"The LUT is not just a compliance formality it's a strategic working capital tool. File early, document meticulously, and treat export timelines as non-negotiable. For a seamless experience, leverage professional platforms like Taxoreo (www.taxoreo.com) to manage your GST filings and ensure your business stays audit-ready."

📚 Official References (For Verification)

- Rule 96A, CGST Rules, 2017: Refund of integrated tax paid on goods or services exported under bond or LUT.

- Section 16, IGST Act, 2017: Framework for Zero-rated supplies.

- CBIC Circular No. 8/8/2017-GST: Guidance on the extension of LUT facilities.

- GST Portal User Guide: Official steps for furnishing Form RFD-11.

- Notification No. 16/2017-Central Tax: Established the LUT procedural framework.

About This Content: This guide was created using verified information from CBIC notifications and GST rules as of March 2026. For end-to-end support with GST, taxation, and business registrations in India, Taxoreo is your trusted partner, providing expert guidance and affordable compliance services